》View SMM Lead Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Database

SMM, February 21:

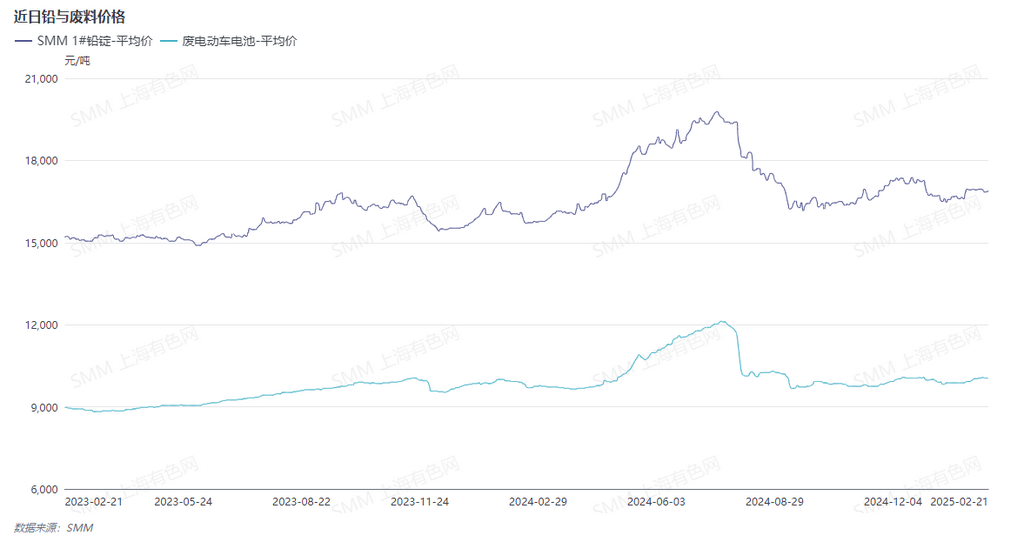

As February draws to a close, the resumption progress of secondary lead smelters has become the focus of market attention. This week, lead prices declined, mainly due to bearish factors stemming from weak end-use consumption. The operating rates of downstream battery producers remained low, leading to sluggish demand for lead ingot procurement. Additionally, after March, the lead-acid battery replacement market will enter its traditional off-season, prompting producers to prefer producing based on sales, which may further limit the upward potential of lead prices.

Meanwhile, the demand for scrap lead-acid batteries surged due to the concentrated resumption of secondary lead smelters. The accelerated post-holiday resumption of secondary lead smelters significantly increased the demand for scrap lead-acid batteries, resulting in a notable expectation of price hikes. At the same time, smelters are facing heightened cost pressure, with rising raw material costs and subdued selling prices narrowing their profit margins, pushing some smelters into a loss-making state.

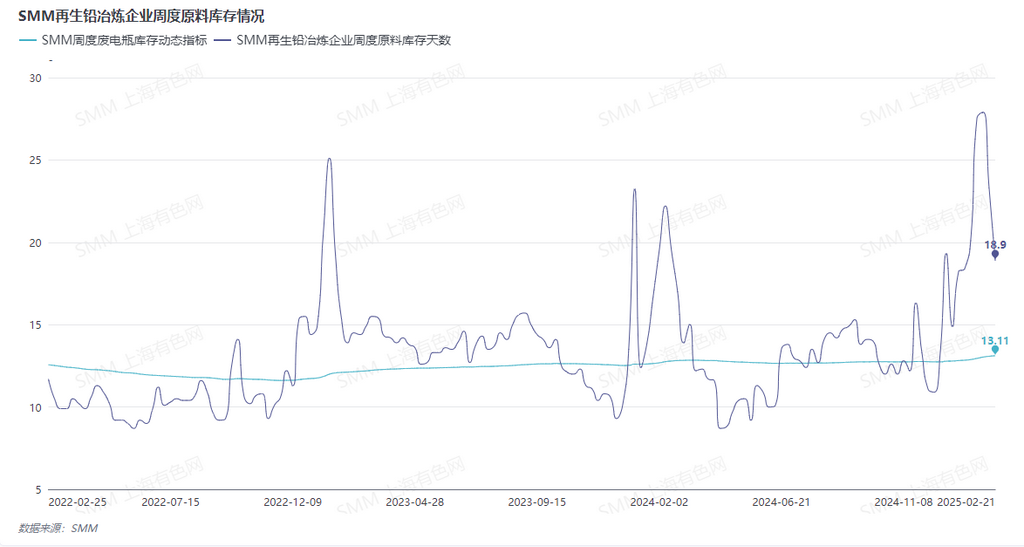

This week, scrap battery recyclers, fearing price drops, opted to sell off, temporarily improving the arrivals of raw materials at secondary lead smelters. However, this phenomenon did not last. With the accelerated resumption of secondary lead production, the days of scrap inventories dropped sharply, reflecting the market's urgent demand for raw materials.

Overall, the secondary lead market presents a complex situation: on one hand, the support from recycling costs; on the other hand, bearish pressure from weak consumption. This tug-of-war between sellers and buyers has kept lead prices in a high-level consolidation trend. Market participants need to closely monitor subsequent supply and demand changes to respond to potential price fluctuations.